-- Why A Major Federal Debt Crisis Could Be a Long Way Off

Past Viewpoints:The Age of AI: An Optimistic View

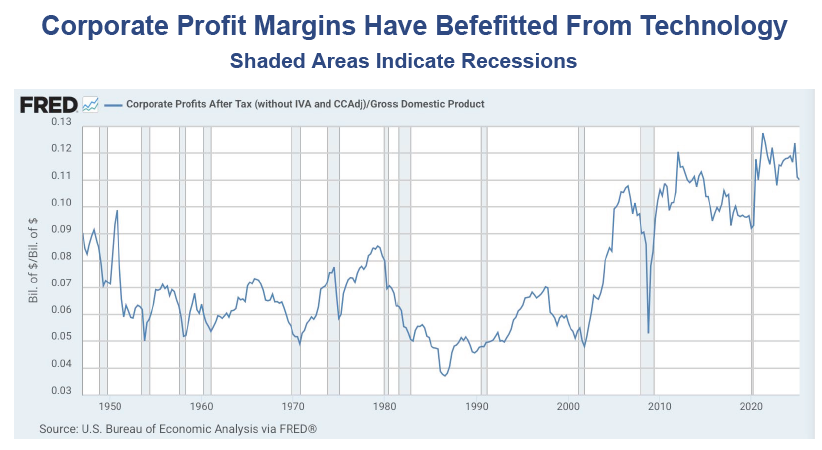

We’ve all heard the doomsday scenarios. But as Artificial Intelligence (AI) technology goes mainstream over the next 20 years, it also has the potential to unlock a period of prosperity. I know predicting the future is a nearly impossible task. Still, the impacts of the industrial era, electricity, radio, television, semiconductors, computers, mobile phones and the Internet are well-known. Over time, advancing technology has a way of taking ideas that are impossible or expensive, and making them relatively cheap and affordable. By progressively automating a greater share of human activities, it has boosted corporate profitability, and by creating new ways to do things it has put downward pressure on inflation.

AI will likely do more of the same, perhaps while taking automation to a whole new level. In the past, advancing technology has tended to create more jobs than it displaces. But given the potential for relatively fast adoption and the likelihood of rapidly-growing capabilities, that may not be the case this time around. Some technology leaders have speculated that many of today’s jobs could eventually become unnecessary. That may be true, but services that were not previously possible will create new work opportunities, as will an expanding "gig" economy (where anyone with intellectual property or a physical asset – property, vehicle, computer, robot, machine – can create an income steam out of it). Still, the very nature of employment could see a big impact, and it’s within the realm of possibilities that a majority of people who work could end up being proprietors who work for themselves.

With those thoughts in mind, what should investors expect as AI technology goes mainstream?

Robust Productivity and Reduced Inflation RiskWe already know that AI can write software, and that it’s capability for doing so is rapidly improving. That alone will be enough to create a noticeable improvement in service-sector productivity. As the technology’s capabilities improve, allowing other types of white-collar job functions to become more automated, service-sector productivity could approach that of manufacturing. A scenario like that would put significant downward pressure on inflation. Steeper Yield Curve; Reduced Recession Risk

Periods of elevated productivity tend to push up borrowing demand, because companies are often making larger than usual capital investments. That tends to pull up the long end of the yield curve. At the same time, the reduced threat of inflation allows for the Fed to reduce short-term interest rates. While the link between the yield curve and recession risk is not as strong as it once was, a steeper yield curve in combination with heavy business spending could reduce the risk of a recession (GDP contraction for two quarters in a row).

Some technology corporations that employ hundreds (or thousands) of software developers have begun modest layoffs in recent years. It’s not because of weak business conditions. Rather, it’s the realization that more projects can be done with fewer workers thanks to AI. As this becomes the norm in other types of white-collar job functions, it will spread to other industry groups, as is currently happening in the automotive sector. Higher P/E Ratios Driven By Rising Profit Margins

If corporations are able to accommodate revenue growth without having to do as much hiring, profit margins may continue to rise, and if they do, P/E ratios could settle into a higher range as well (a growing technology weighting within the S&P 500 has already contributed to this effect). In a scenario like this, a high multiple for the stock market would not necessarily spell trouble like it sometimes has in the past. Renaissance For Active Management?

Over the last year, some of Fidelity’s active sector funds have shown improved performance relative to their benchmarks, especially in industry groups where AI is creating substantial opportunities for revenue growth and/or cost reduction. This may be due in part to divergences within analyst projections. In an environment where there is less consensus about the future, the market may be slow to recognize emerging trends, creating opportunities for smart active managers. Another consideration is the big difference in valuations between large-caps and smaller stocks (which is mainly the result of big differences in profit margins). If AI is able to narrow this valuation gap by leveling the playing field from a labor-efficiency standpoint, any improvement in mid-cap and small-cap performance could also serve as a tailwind for actively managed funds that invest in smaller stocks.

As always, big periods of change often come with unique risks that are not easily anticipated. It is impossible to know what will cause the next bear market. Heavy-handled

AI regulations in foreign countries? A domestic political crisis surrounding AI’s impact on the job market? Higher corporate taxes? A cryptocurrency crash? Anything is possible. But given the potential for a long period where corporate earnings are growing at faster than historical rates, the stock market of the next 20 years is likely a long-term risk worth taking, even if there are big issues looming along the way.

Third Quarter ReviewInflation readings did not move much in the third quarter. Meanwhile, the job market weakened considerably, creating the necessary headroom for the Fed to resume its cycle of interest rate cuts. Stocks rallied, helped along by solid earnings results and a favorable earnings outlook. The S&P 500 climbed 8.1%, bringing its year-to-date gain to 14.8%.

Bonds edged up as well, thanks to a drop in consumer borrowing demand (which was reflected in part by an unexpected decline in mortgage rates). Plus, fixed-income investors appeared willing to look past continuing Federal deficits, made slightly worse by the passage of Trump’s tax package. The U.S. Aggregate Index rose 2.0% for the quarter, gaining 6.1% year-to-date. On the stock side, our sector holdings outperformed, while our diversified portfolios were mixed, with most finishing slightly ahead or slightly behind the S&P 500. We trailed on the bond side due to our emphasis on intermediate and shorter-maturity funds, which didn’t benefit as much from the decline in longer-term interest rates.

Looking AheadThe prospect of increased profit margins (as corporations embrace AI technology) has pushed the S&P 500’s trailing P/E ratio up near the 30 mark, a level the index hasn’t seen for nearly five years. Some find this concerning, but it simply reflects the more favorable earnings environment that companies will likely face in future years, which for many could mean the ability to grow revenue while keeping costs relatively flat.

The market has priced in two more quarter-point interest rate cuts between now and the end of the year, with an easing move in November now viewed as a near certainty because of the weakening job market and the effects of the government shutdown. At the same time, business spending remains robust, suggesting that corporate CEOs are anything but bearish.

As always, we’ll be looking for opportunities to improve our portfolio positioning as the situation evolves. On the stock side, we’ll be looking to add to our mid-cap and/or small-cap positions if conditions continue to improve for smaller companies. We have no immediate plans to change our bond positioning, but at some point it could make sense to move further out on the yield curve.

Sincerely,

Jack Bowers

President & Chief Investment Officer