-- Why A Major Federal Debt Crisis Could Be a Long Way Off

Past Viewpoints:An Important Milestone For The Future of Energy

NV Energy’s Gemini Project, potentially the largest U.S. solar farm upon completion in 2023, is about to be given the green light. Some 690 Megawatts of photovoltaic solar panels would be installed on 7,100 acres of Federal land in the Nevada desert about 35 miles Northeast of Las Vegas. The project includes 1,520 MWh of battery storage, allowing the power plant to deliver electricity during high-demand periods after sunset.

The solar output from Gemini, in combination with that of two other planned solar farms, could account for some 15% of NV Energy’s statewide power production, putting the utility six years ahead of schedule for meeting a 2030 mandate requiring 50% of power generation from renewable sources. The utility now has a long-term goal of generating 100% of its power from renewable sources, implying that most of its natural gas plants (which form the backbone of the Nevada grid today) would eventually be idled.

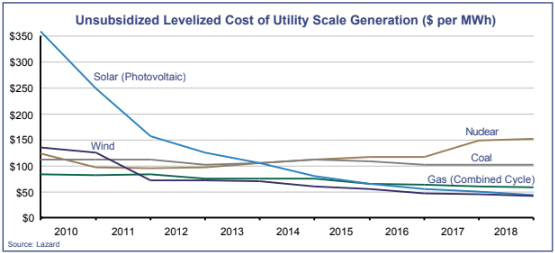

Making all this possible: plunging photovoltaic solar panel costs, which have shrunk by over a factor of ten during the last decade. Even with the added cost of battery storage, the overall cost of power generated at the Gemini plant is expected to be less than that of natural gas plants operating today.

It’s interesting how low-cost technology can force an unlikely cast of characters to walk the line. In this case, Berkshire Hathaway’s Mid-American Energy has made a renewable energy U-turn just five years after it bought out NV Energy and convinced the state’s utility board to kill Nevada’s roof-top solar program (a move that angered the utility’s customer base and led to the voter-approved renewable power mandate). And because the project is on Federal land, it must be approved by President Trump, who has refused to exempt imported solar panels from an existing 25% tariff, and is determined to let all Federal subsidies for renewable power expire this year. Not to worry; despite his pro-coal stance, he’s already supported two similar power plants, and he’s expected to approve this one too.

Battery Storage is Key

Until recently the idea of a 100% renewable power grid was pie-in-sky. But now that utility-scale lithium battery storage has been proven (Tesla’s 2017 Hornsdale project in Australia has prevented blackouts while earning a high return on investment), there really aren’t any limitations. Wherever there is wind or sun, power can be generated and stored - in most cases at a price that’s competitive with today’s fossil fuel power plants. The amount of land required is relatively small percentage-wise. For Nevada, a solar generation area roughly 12 miles by 12 miles would cover state-wide power demand. For the U.S. it could be done with 0.6% of the available land (less if off-shore wind and rooftop solar are fully deployed). It’s a lot of area compared with the way that power is generated today. But it would be cheap and carbon-free.

Reducing Climate Change Risk

With an established cost-effective renewable power model now in hand, global power providers can likely get to 90% renewable power over the next 2-3 decades. And with the substantial cost advantage of electrified transportation already disrupting at an accelerated pace, the percentage of passenger and freight miles powered by electric drive are also likely to be above 90% by the time the grid gets there (ships and aircraft are only 5% of global carbon emissions). There will be no additional electricity required for powering world’s transportation system, because the electricity we use today to extract and refine motor fuels will do the trick. There may even be a net reduction, because some vehicle charging stations (and some vehicles) will be powered in part by on site or in-vehicle solar panels. For the small portion of the global economy that must still run on hydrocarbons, carbon-neutral fuels (where biogas is the feedstock) hold the key. Some airlines are already moving in that direction for marketing advantage. As for dealing with elevated levels of CO2 and methane, it could be as simple as planting more trees and deploying satellite-based solar reflectors (blocking 1% of sunlight reaching the earth would be more than enough). Odds are there will be many cost-effective technology solutions in the next 20 years.

Stock Market Implications

With the media making it sound like we’re all doomed, the stock market is starting to mark down corporations that have perceived climate change liability. As for the broad U.S. market, impacts to GDP growth, inflation, and corporate earnings have so far been limited, with no discernible impact on P/E ratios. That may change if new draconian measures are enacted by governments of the world’s leading economies, but it seems less likely at this point. As long as carbon emissions keep declining from technological change, regulators can stand back and let the free markets take care of the problem.

Still, there will be energy and transportation disruption casualties. The decline of fossil-fuel power generation on the global grid has already wiped out most of GE’s dividend, and Tesla is poised to disrupt the auto industry much like Amazon disrupted the retail industry. Many regulated utilities will be forced to shrink as their industrial customers install their own solar generation. Oil and gas production could fall by a factor of ten as fuel demand disappears. Ditto for coal, which in the future will have little purpose other than for steel production.

But even as all this plays out, there will be many winners as the cost of transporting people and freight falls dramatically in an electric (and largely autonomous) age. Long-term investors should not shy away from investing in stocks due to climate change risk, because the solutions are now in hand – we just need a few decades (and a lot of capital) to fully implement them.

Fourth Quarter Review

A surprising amount of trade uncertainty was removed during the fourth quarter. In early December, the U.S. and China reached a phase-one accord on trade, canceling new tariffs and partially rolling back existing ones. Separately, Congressional leaders came to agreement on an updated version of NAFTA. And with U.K. election results heavily favoring Boris Johnson and the Conservative Party, the stage now appears set for an orderly Brexit and a trade agreement with the U.S.

In another favorable development cheered by stock investors, Fed Open Market Committee members became unified around a policy of holding interest rates steady in 2020, while standing ready to ease if the economy weakens. The dovish shift greatly reduces recession risk.

Together these developments led to a broad rally among stocks, both foreign and domestic. The S&P 500 jumped 9.1% for the quarter, finishing 2019 with a gain of 31.5%. Most of our stock-oriented portfolios outperformed for the quarter, though some fell slightly short of the S&P 500 for the year. Throughout the quarter we continued our heavy emphasis on U.S. growth stocks, especially the technology sector.

The bond market often loses out during strong periods for stocks. But thanks to improving credit conditions, losses were effectively limited to long-duration government bond funds. The Barclay’s Aggregate Bond Index finished just ahead of breakeven for the quarter (up 0.2%), finishing the year with an 8.7% return. The income side of our portfolios did slightly better, while also outperforming for the full year.

Outlook

Until recently, about one-third of economists had expected a recession to take hold in 2020, meaning two or more consecutive quarters of negative GDP growth. But now, with the trade situation improving, and reduced mortgage rates spurring more home construction activity, the threat of a recession has been taken off the table for the most part. The latest economic forecasts call for U.S. GDP growth of around 2% for 2020. While that’s on the low end compared with the run rate we’ve seen since the beginning of 2016, it’s strong enough that wage growth is likely to remain robust in today’s tight labor market. Those wage gains, in turn, are poised to keep consumers spending at a healthy clip in 2020 – most likely offsetting any continued weakness in business and investment spending.

While it’s highly unlikely that 2020 will bring a repeat of the strong stock-market gains that occurred last year, better trade conditions could set the stage for improved corporate earnings growth. While most of the market’s gain in 2019 was due to P/E expansion (reversing the P/E contraction that occurred in late 2018), the operating earnings ratio currently stands at about 20, right in line with its 25-year average. Although some growth stocks appear pricey, and many value stocks appear cheap, the market overall seems priced about right for expected levels of inflation and interest rates.

Our portfolios remain heavily growth-oriented, although for 2020 we have our eye on boosting exposure to value stocks, both foreign and domestic. Value stocks have performed poorly over the last decade, but investors are now beginning to question the extent of technology disruption (as evidenced by notable 2019 stock gains for Target Stores, Disney, and Marriott). As for foreign markets, many stand to benefit from improving trade. And because stock values are cheaper, and trade has greater impact on GDP growth, the opportunities could rival U.S. stocks.

Sincerely,

Jack Bowers

President & Chief Investment Officer