-- Why A Major Federal Debt Crisis Could Be a Long Way Off

Past Viewpoints:Update: Does It Make Sense To Roth-Convert

Your IRA In Retirement?

You’ve got a significant amount of money in a traditional (or rollover) IRA, and you’re not thrilled with RMDs (Required Minimum Distributions) that get bigger with each passing year. Does it make sense to “pre-pay” the entire tax liability so that the account can grow tax-free for the rest of your life, and for up to another 10 years after it’s passed on to your non-spouse heirs?

It’s not an easy question to answer, but with the possibility of future tax rates rising, the idea of doing a Roth conversion is looking more attractive. Your heirs may still be required to distribute inherited IRA assets within 10 years, but at least with tax-free Roth distributions they won’t have to pay tax on them.

Deciding whether to do a Roth conversion (an option that is open to anyone) is not just about estate planning. To get an idea of whether it makes sense for your situation, consider the following questions: (1) Am I in reasonably good health for my age? (2) Can I pay the conversion tax bill (which will likely range from 25-50% of the amount converted) from non-IRA sources and avoid living expense draws on the Roth account for at least 10 years? (3) Am I okay with the higher Medicare Part B premiums that might result two years down the road? (4) Will it matter if a Roth account makes it more difficult to qualify for Medicaid if I need to go into assisted living? (5) Can I do the conversion at a time when my capital gain exposure is low, and without pushing myself into a tax bracket that is much higher than what I expect for my future retirement years? If you answered yes to all of these questions, you may want to consider a Roth conversion.

Regarding that last question, Roth conversions can be done in stages. You can convert portions of an account, matching the added tax liability with years when capital gain exposure is low (or avoiding years when college-age children may need financial aid). If you have plans for IRA charity donations, don’t convert that money because it can already be donated free of tax liability

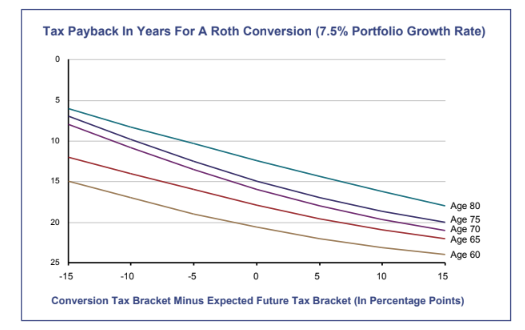

The chart below can give you an idea of what the payback period is for the tax bill that would result from a Roth conversion. The major factors affecting the tax recovery period are taxbrackets and age. Portfolio growth rate matters too, but the impact is relatively mild, so for the sake of simplicity we’re only showing what happens for a 7.5% portfolio growth rate. We’ve assumed that non-IRA money is used to pay the conversion cost so that the full value of the IRA is available to compound tax-free in Roth form.

While there should be no surprise that the payback is longer when your conversion tax bracket is higher than your expected future retirement tax bracket, the impact of age is somewhat counter-intuitive. At age 60, you are bearing the cost of conversion but seeing no payback on future tax savings for at least 12 years. That’s because RMDs don’t kick in until after age 72. Why not just wait? Well, if your traditional IRA is large, you might need to spread the conversion out over a long period of time to keep your tax bracket from climbing too high. At age 80, payback times are shorter. That’s because RMDs are based on life expectancy, which means they get a lot bigger above age 80, greatly increasing the tax liability of a traditional IRA. Because a Roth conversion eliminates RMDs just as the resulting tax bite starts to become rather large, the resulting payback is relatively short at this age (provided the conversion doesn’t push your tax bracket up too high).

Fourth Quarter ReviewThe unexpected combination of unusually strong GDP and declining inflation prompted the Fed to signal an early end to its string of tightening moves in the fourth quarter. This seemingly contradictory situation occurred thanks to robust exports of domestic shale oil and LNG, which pushed down global energy prices while reducing domestic inflation and boosting domestic GDP. But an expanding labor force and rising productivity helped as well.

Investors, many of whom spent much of 2023 building up their cash reserves to take advantage of 5% money market rates, suddenly wanted to buy stocks and bonds again, and began doing so in earnest during November and December. For the fourth quarter, the S&P 500 surged 11.7%, bringing its 2023 gain to 26.3%. On the bond side, the Bloomberg Barclay’s U.S. Aggregate jumped 6.8% to finish with a 5.5% return for the year.

Performance-wise, our sector holdings kept up with S&P 500, but our diversified stock fund bets trailed slightly behind the index due to a greater emphasis on value stocks. We also lagged on the bond side, because the actions we took in October to limit our interest-rate exposure ended up holding us back somewhat when bonds rallied in the final weeks of the year.

OutlookSome economists are still calling for a mild recession this year, but it’s mainly those who probably have too much faith in the yield curve indicator (some are also largely ignoring the growing role that energy exports play in determining U.S. GDP). We don’t think a recession is in the cards. Consumers will likely keep spending thanks to the wealth effect, while business keep investing in factories, clean energy and artificial intelligence.

Expect Inflation to return to a normal 2% level in 2024. Why? The money supply stopped expanding 18 months ago, supply chains have returned to normal and the labor force participation rate is rebounding to its pre-pandemic level of around 63%. And recent declines in oil and LNG prices are likely to persist for most of the coming year, thanks to continued weakness in China’s economy and growth in energy exports among non-OPEC countries. The Fed will likely follow through on its recent dot-plot of expectations by cutting short-term interest rates several times in 2024.

It still isn’t clear what will happen at the long end of the yield curve as the financing needs of the federal government weigh off against a weaker global economy and shrinking foreign demand for U.S. Treasuries. At some point it could make sense for us to exit our defensive bond positioning, but we plan to move cautiously.

As for stocks, the AI rally that took the Magnificent Seven stocks to a 30% weight in the S&P 500 seems fully priced in. While this group of stocks may continue to lead the market, value stocks could steal the show as borrowing costs start to come down. Our portfolios are reasonably well-balanced between growth and value stocks, but we may need to boost our value exposure at some point.

Finally, a warning about overly-popular inflation hedges such as bitcoin and gold. For the former, performance expectations are unrealistically high regarding the potential launch of domestic bitcoin ETFs, and for the latter, prices for are elevated because China’s central bank is by far the world’s biggest buyer of gold. Stocks and bonds are a better way to hedge against inflation, so we have no plans to speculate in these areas. For those who are doing so on their own, we suggest limiting crypto-currencies to 1% or less of total holdings, and limiting gold and gold stocks to a weighting of 5% or less.

Sincerely,

Jack Bowers

President & Chief Investment Officer